Why should a man intentionally live his life with one kind of anxiety followed by another?

—Imbolo Mbue

Anxiety is perhaps the best way to describe the attitude that dominated the minds of investors and the general public toward financial markets by the end of 2008. The 2008 financial crisis is considered by numerous economists to have been the worst financial crisis since the Great Depression. The years leading up to the crisis saw a flood of irresponsible mortgage lending and a massive systemic failure of financial regulation and supervision. The fallout was so immense that it threatened the collapse of large financial institutions. National governments had to intercede to bail out major banks. This chapter begins with a discussion about the 2008 financial crisis, and then we discuss the aftermath, which led to an environment where a new banking system and alternative currency such as Bitcoin could thrive. Then, we dive into the technology stack that powers Bitcoin. Remarkably, the components of this stack are not entirely new, but they are strung together in an ingenious design. Finally, we end the discussion by talking about the heightened interest in blockchain, a major technical breakthrough that has the potential to revolutionize several industries.

Paradigm Shift

Revolutions often look chaotic, but this one was brewing quietly, headed by an unknown individual under the name Satoshi Nakamoto, who dreamed of changing the financial world. Any number of parties can be blamed for the financial crisis, but the common denominator was that fundamental financial and accounting instruments used to maintain integrity of the entire system became too complex to be used efficiently. Trust, the ultimate adhesive of all financial systems, began to disappear in 2008. The regulations have since changed to prevent similar circumstances from arising, but it was clear that there was a need for autoregulation of trust between counterparties and transparency into their ability to enter any type of a sales contract. A counterparty is essentially the other party in a financial transaction. In other words, it is the buyer matched to a seller. In financial transactions, one of the many risks involved is called counterparty risk, the risk that each party involved in a contract might not be able to fulfill its side of the agreement. The systemic failure referenced earlier can now be understood in terms of counterparty risk: Both parties in the transaction were accumulating massive counterparty risk, and in the end, both parties collapsed under the terms of the contract. Imagine a similar transaction scenario involving multiple parties, and now imagine that every single player in this scenario is a major bank or insurance company that further serves millions of customers. This is just what happened during the 2008 crisis.

© Vikram Dhillon, David Metcalf, and Max Hooper 2017

1

V. Dhillon et al., Blockchain Enabled Applications, https://doi.org/10.1007/978-1-4842-3081-7_1

Chapter 1 ■ Behold the dreamers

The next issue we need to discuss is that of double spending. We revisit this topic again strictly in the context of Bitcoin, but let’s get a basic understanding of the concept by applying it to the financial crisis. The principle behind double spending is that resources committed to one domain (e.g., one transaction) cannot also be simulataneously committed to a second disparate domain. This concept has obvious implications for digital currencies, but it can also summarize some of the problems during the 2008 crisis.

Here’s how it started: Loans (in the form of mortages) were given to borrowers with poor credit histories who struggled to repay them. These high-risk mortgages were sold to financial experts at the big banks, who packaged them into low-risk public stocks by putting large numbers of them together in pools.

This type of pooling would work when the risks associated with each loan (mortgage) are not correlated.

The experts at big banks hypothesized that property values in different cities across the country would change independently and therefore pooling would not be risky. This proved to be a massive mistake. The pooled mortage packages were then used to purchase a type of stock called collateralized debt obligations (CDOs). The CDOs were divided into tiers and sold to investors. The tiers were ranked and rated by financial standards agencies and investors bought the safest tiers based on those ratings. Once the U.S.

housing market turned, it set off a domino effect, destroying everything in the way. The CDOs turned out to be worthless, despite the ratings. The pooled mortgages collapsed in value and all the packages being sold instantly vaporized. Throughout this complex string of transactions, every sale increased the risk and incurred double spending at multiple levels. Eventually, the system equilibrated, only to find massive gaps, and collapsed under the weight. Following is a brief timeline for 2008. (This timeline was made following a presentation by Micah Winkelspech at Distributed Health, 2016).

• January 11: Bank of America buys the struggling Countrywide.

• March 16: Fed forces the sale of Bear Stearns.

• September 15: Lehman Brothers files for Chapter 11 bankruptcy.

• September 16: Fed bails out American International Group (AIG) for $85 billion.

• September 25: Washington Mutual fails.

• September 29: Financial markets crash; the Dow Jones Industrial Average fell 777.68

points and the whole system was on the brink of collapse.

• October 3: U.S. government authorizes $700 billion for bank bailouts.

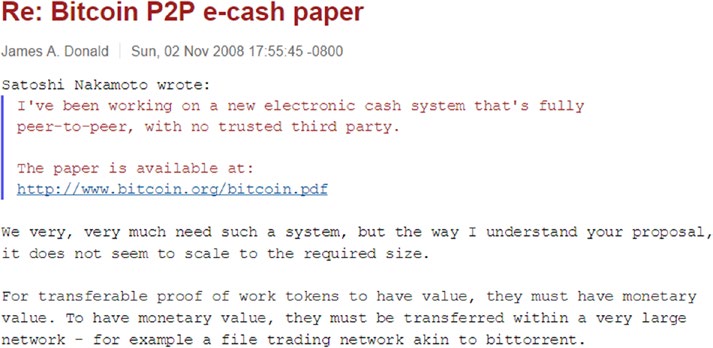

The bailout had massive economic consequences, but more important, it created the type of environment that would allow for Bitcoin to flourish. In November 2008, a paper was posted on the Cryptography and Cryptography Policy Mailing List titled “Bitcoin: A Peer-to-Peer Electronic Cash System, ”

with a single author named Satoshi Nakamoto. This paper detailed the Bitcoin protocol and along with it came the original code for early versions of Bitcoin. In some manner, this paper was a response to the economic crash that had just happened, but it would be some time before this technological revolution caught on. Some developers were concerned with this electronic cash system failing before it could ever take hold and their concern was scalability, as pointed out in Figure 1-1.

2

Chapter 1 ■ Behold the dreamers

Figure 1-1. Initial reception of the Bitcoin protocol included concerns about scalability and realistic prospects for Bitcoin

So who is Nakamoto? What is his background? The short and simple answer is that we don’t know. In fact, it is presumptuous to assume that he is actually a “he.” The name Satoshi Nakamoto was larely used as a pseudonym and he could have been a she, or even a they. Several reporters and news outlets have dedicated time and energy to digital forensics to narrow down candidates and find out the real identity of Nakamoto, but all the efforts so far have been wild-goose chases. In this case, the community is starting to realize that maybe it doesn’t matter who Nakamoto is, because the nature of open source almost makes it irrelavent.

Jeff Garzik, one of the most respected developers in the Bitcoin community, described it as follows: “Satoshi published an open source system for the purpose that you didn’t have to know who he was, and trust who he was, or care about his knowledge.” The true spirit of open source makes it so that the code speaks for itself, without any intervention from the creator or programmer.

Cypherpunk Community

Nakamoto’s real genius in creating the Bitcoin protocol was solving the Byzantine generals’ problem.

The solution was generalized with components and ideas borrowed from the cypherpunk community.

We briefly talk about three of those ideas and the components they provided for the complete Bitcoin protocol: Hashcash for proof of work, Byzantine fault tolerance for the decentralized network, and blockchain to remove the need for centralized trust or a central authority. Let’s dive into each one, starting with Hashcash.

Hashcash was devised by Adam Black in the late 1990s to limit e-mail spam with the first of its kind Proof-of-Work (PoW) algorithm. The rationale behind Hashcash was to attach some computational cost to sending e-mails. Spammers have a business model that relies on sending large numbers of e-mails with very little cost associated with each message. However, if there is even a small cost for each spam e-mail sent, that cost multiplies over thousands of e-mails, making their business unprofitable. Hashcash relies on the idea of cryptographic hash functions: A type of hash function (in the case of Bitcoin, SHA1) takes an input and converts it into a string that generates a message digest, as shown in Figure 1-2. The hash functions are designed to have a property called one-way functions, which implies that a potential input can be verified very easily through the hash function to match the digest, but reproducing the input from the digest is not feasible. The only possible method of re-creating the input is by using brute force to find the appropriate input string. In practice, this is the computationally intensive element of Hashcash and also eventually Bitcoin. This principle has become the foundation behind PoW algorithms powering Bitcoin today and most cryptocurrencies. The PoW for Bitcoin is more complex and involves new components, which we talk about at length in a later chapter.

3

Chapter 1 ■ Behold the dreamers

Figure 1-2. Mechanism of a cryptographic hash function. It takes an input and consistently converts it to a string of an output digest.

The next idea we need to discuss is the Byzantine generals’ problem. It is an agreement problem among a group of generals, with each one commanding a portion of the Byzantine army, ready to attack a city. These generals need to formulate a strategy for attacking the city and communicate it to each other adequately. The key is that every general agrees on a common decision, because a tepid attack by a few generals would be worse than a coordinated attack or a coordinated retreat. The crux of the problem is that some of the generals are traitorous. They might cast a vote to deceive the other generals and ultimately lead to a suboptimal strategy. Let’s take a look at an example: In a case of odd-numbered generals, say seven, three support attacking and three support retreat. The seventh general might communicate an agreement to the generals in favor of retreat, and an agreement to attack to the other generals, causing the whole arrangement to fall apart. The attacking forces fail to capture the city because no intrinsic central authority could verify the presence of trust among all seven generals.

In this scenario, Byzantine fault tolerance can be achieved if all the loyal generals can communicate effectively to reach an undisputed agreement on their strategy. If so, the misleading (faulty) vote by the traitorous general would be revealed and fail to perturb the system as a whole. For the Bitcoin protocol, Nakamoto’s key innovation to enable Byzantine fault tolerance was to create a peer-to-peer network with a ledger that could record and verify a majority approval, thereby revealing any false (traitorous) transactions. This ledger provided a consistent means of communication and further allowed for removal of trust from the whole system.

The ledger is also known as the blockchain, and by attaching blockchain to Bitcoin, it became the first digital currency to solve the double spending problem network-wide. In the remainder of this chapter, we present a broad overview of the broad overview of the technology, and the concept of a blockchain-enabled application.

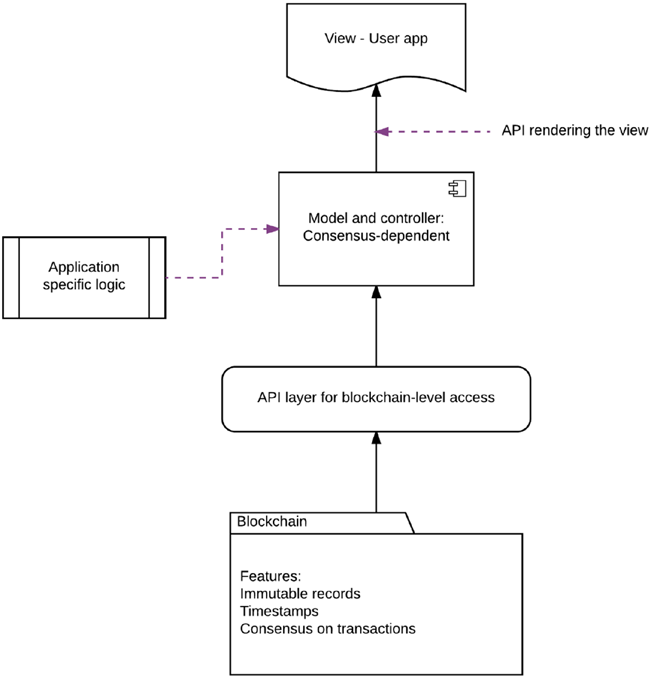

The blockchain is primarily a recording ledger that provides all involved parties with a secure and synchronized record of transactions from start to finish. A blockchain can record hundreds of transactions very rapidly, and has several cryptographic measures intrinsic to its design for data security, consistency, and validation. Similar transactions on the blockchain are pooled together into a functional unit called a block and then sealed with a timestamp (a cryptographic fingerprint) that links the current block to the one preceding it. This creates an irreversible and tamper-evident string of blocks connected together by timestamps, conveniently called a blockchain. The architecture of blockchain is such that every transaction is very rapidly verified by all members of the network. Members also contain an up-to-date copy of the blockchain locally, which allows for consensus to be reached within the decentralized network. Features such as immutable record-keeping and network-wide consensus can be integrated into a stack to develop new types of applications called decentralized apps (DApps). Let’s look at a prototype of a DApp in Figure 1-3, in the context of the Model-View-Controller (MVC) framework.

■ Note the first block of the blockchain is called the Genesis block. this block is unique in that it does not link to any blocks preceeding it. Nakmoto added a bit of historical information to this block as context for the current financial environment in the United Kingdom: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks. “this block not only proves that no bitcoins existed before January 3, 2009, but also gives a little insight into the mind of the creators.

4

Chapter 1 ■ Behold the dreamers

Figure 1-3. Simple prototype of a decentralized application that interacts with the end user at the final steps The model and controller here rely on the blockchain for data (data integrity and security) and accordingly update the view for the end user. The secret sauce in this prototype is the application programming interface (API), which works to pull information from the blockchain and provides it to the model and controller. This API provides opportunities to extend business logic and add it to the blockchain, along with basic operations that take blocks as input and provide answers to binary questions. The blockchain could eventually have more features, such as oracles that can verify external data and timestamp it on the blockchain itself. Once a decentralized app starts dealing with large amounts of live data and sophisticated business logic, we can classify it as a blockchain-enabled application.

Summary

In this chapter, we started talking about the history of Bitcoin and the financial environment at the time it came into being. We continue our discussion of blockchain and specific features of the peer-to-peer network such as miners and more in the upcoming chapters. The references used in this chapter are available at the end of the book.

5

The Gold Rush: Mining Bitcoin

During the Gold Rush, most would-be miners lost money, but people who sold them

picks, shovels, tents and blue-jeans (Levi Strauss) made a nice profit.

—Peter Lynch

Mining is a foundational concept in understanding how the Bitcoin protocol operates. It refers to a decentralized review process performed on each block of the blockchain to reach consensus without the need for a central authority to provide trust. In other words, mining is the computational equivalent of peer review in a decentralized environment where neither party involved trusts the other. We continue our discussion of a hash-function explained in Chapter 1 as it refers to mining and solving PoW functions.

Then, we integrate the concepts of block target values and network difficulty with mining and how mining has evolved to keep up with the increasing difficulty. This will lead us further into talking about the types of hardware mining that have recently been developed. We end the chapter with an analysis of startups that began selling dedicated hardware for mining, leading to the Bitcoin mining arms race and their eventual failure.

Reaching Consensus

Mining is central to the Bitcoin protocol and has two primary roles: adding new bitcoins to the money supply and verifying transactions. In this chapter, we look at the mechanisms behind these two processes.

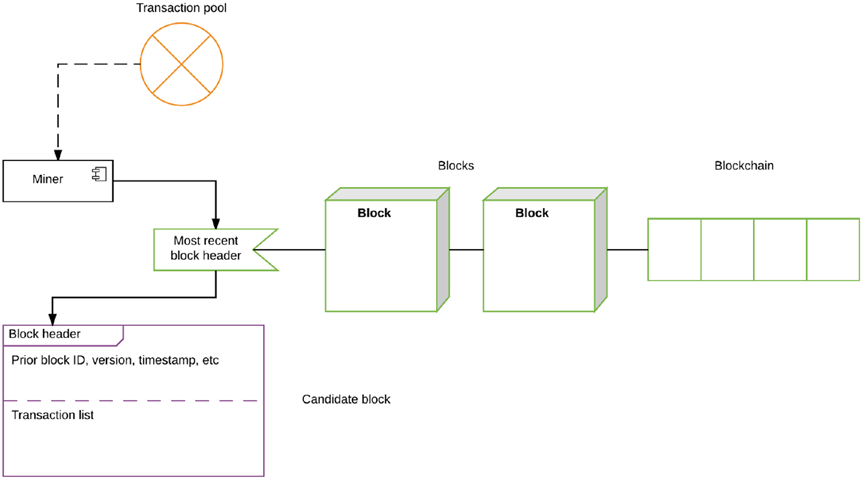

Essentially, mining is the appropriate solution to the double spending problem we discussed previously. To remove the need for a central authority, individuals running the Bitcoin client on their own machines (called miners) participate in the network and verify that transactions taking place between two parties are not fraudulent. Mining is actually a computationally intensive activity, but what incentives does anyone have to help mine for new Bitcoins? The key incentive for miners is getting a reward in the form of Bitcoins for their participation. Let’s look at a simplified view of the mining process in Figure 2-1.

© Vikram Dhillon, David Metcalf, and Max Hooper 2017

7

V. Dhillon et al., Blockchain Enabled Applications, https://doi.org/10.1007/978-1-4842-3081-7_2

Chapter 2 ■ the Gold rush: MininG BitCoin

Figure 2-1. A simplified overview of the mining process

Unpackaged transactions that have recently occurred in the Bitcoin network remain in the transaction pool until they are picked up by a miner to be packaged into a block. A miner selects transactions from the transaction pool to package them in a block. After the block has been created, it needs a header before it can be accepted by the blockchain. Think of this as shipping a package: Once the package has been created, it needs to be stamped so that it can be shipped. A miner uses the header of the most recent block in the blockchain to construct a new header for this current block. The block header also contains other elements such as a timestamp, version of the Bitcoin client, and an ID corresponding to the previous block in the chain. The resulting block is called a candidate block, and it can now be added to the blockchain if a few other conditions are satisfied.

The process of mining is very involved and Figure 2-1 only serves to paint a broad picture regarding the participation of miners in the protocol. Next, we explore the technical aspects of the stamp (analogy referenced earlier) and the mechanism of stamping a package. Keep in mind that mining is a competitive process: Figure 2-1 describes this process for only one miner, but in reality, a very large number of miners participate in the network. The miners compete with each other to find a stamp for the package (block) they created, and the first miner to discover the stamp wins. The race between miners to find a stamp is concluded within ten minutes, and a new race begins in the next ten minutes. Once the stamp is discovered, the miner can complete the block and announce it to the network, and then it can be added to the blockchain. Let’s take a look at the process behind searching for the stamp, better known as a block-header, in Figure 2-2.

8

Chapter 2 ■ the Gold rush: MininG BitCoin

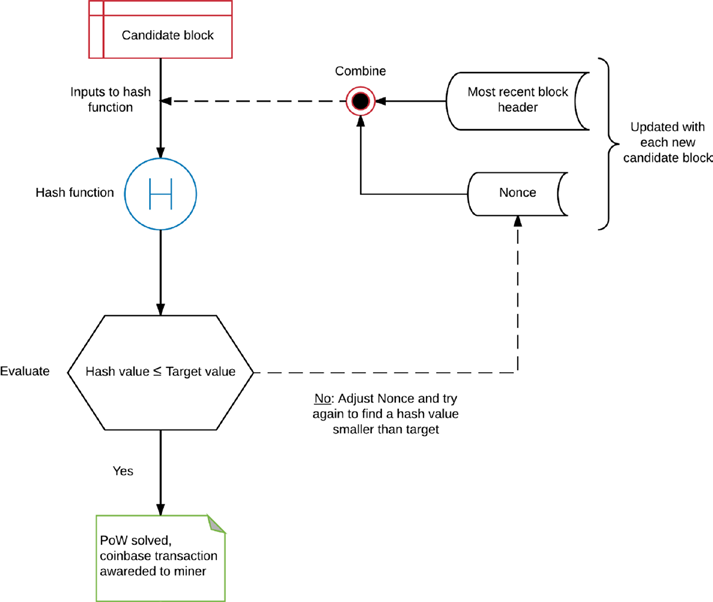

Figure 2-2. Generating a block header by solving proof of work (PoW)

The package created by a miner is almost a block, but it is missing a header. It’s called a candidate block and it can only be added to the blockchain after the stamp, or the header, is added. The header from the most recent block in the blockchain is retrieved and combined with a 32-bit value called nonce. This combination is directed to the hash function (SHA-256) as an input. The hash function computes a new resulting hash as an output. This generated hash is then compared to the target value of the network (at the given time). If the hash value is larger than the target value, then the nonce is readjusted and a new input is sent to the hash function to obtain a new potential output. The problem of finding the appropriate hash value that is smaller than the target value is at the heart of PoW, and it can only be solved using brute force.

Once a hash value smaller than the target value is discovered by a miner, this hash can then be used in the block header for the candidate block. The first miner to discover the hash is considered to be the winner. The winning miner has shown PoW that she did to discover the hash, so the transactions contained within the block are now considered valid. This block can now be added to the blockchain. Additionally, the winning miner also earns the reward for solving the PoW problem, which is a certain number of Bitcoins. This whole process from packaging transactions into a block, to finding the hash and announcing the block to the Bitcoin network repeats itself approximately every ten minutes.

9

Chapter 2 ■ the Gold rush: MininG BitCoin

We introduced some new terminology in Figure 2-2, so let’s describe the terms here properly for the sake of completion.

• Candidate block: An incomplete block, created as a temporary construct by a miner to store transactions from the transaction pool. It becomes a complete block after the header is completed by solving the PoW problem.

• PoW: The problem of discovering a new hash that can be used in the block header of the candidate block. This is a computationally intensive process that involves

evaluating a hash taken from the most recent block and appending a nonce to it

against the target value of the network. This problem can only be solved using brute force; that is, multiple trials of using the hash (from the most recent block header) and nonce being adjusted each time are necessary to solve the PoW problem.

• Nonce: A 32-bit value that is concatenated to the hash from the most recent block header. This value is continuously updated and adjusted for each trial, until a new

hash below the target value is discovered.

• Hash function: A function used to compute a hash. In the Bitcoin protocol, this function is the SHA-256.

• Hash value: The resulting hash output from a hash function.

• Target value: A 265-bit number that all Bitcoin clients share. It is determined by the difficulty, which is discussed shortly.

• Coinbase transaction: The first transaction that is packaged into a block. This is a reward for the miner to mine the PoW solution for the candidate block.

• Block header: The header of a block, which contains many features such as a timestamp, PoW, and more. We describe the block header in more detail in Chapter 3.

■ Note after going over the terms defined above, revisit Figures 2-1 and 2-2. some concepts that were abstract will become clear now and the information will integrate better.

Now that we have a better idea of how mining works, let’s take a look at mining difficulty and target values. Those two concepts are analogous to dials or knobs that can be adjusted over the course of time for the network and all Bitcoin clients update to follow the latest values. So what is mining difficulty?

Essentially, it can be defined as the difficulty of finding a hash below the target value as a miner is solving the PoW problem. An increase in difficulty corresponds to longer time needed to discover the hash and solve PoW, also known as mining time. The ideal mining time is set by the network to be approximately ten minutes, which implies that a new block is announced on the network every ten minutes. The mining time is dependent on three factors: the target value, the number of miners in the network, and mining difficulty.

Let’s look at how these factors are interconnected.

1.

An increase in mining difficulty causes a decrease in the target value to

compensate for the mining time.

2.

An increase in the number of miners joining the network causes an increase in

the rate at which PoW is solved, decreasing the mining time. To adjust for this,

mining difficulty increases and the block creation rate returns to normal.

3.

The target value is recalculated and adjusted every 2,016 blocks created, which

happens in approximately two weeks.

10

Chapter 2 ■ the Gold rush: MininG BitCoin

As we can see, there is a common theme of self-correction in the Bitcoin network that allows it to be very resilient. Miners are the heartbeat of the Bitcoin network and they have two main incentives for participation:

• The first transaction to be packaged in a block is called the coinbase transaction.

This transaction is the reward that the winning miner receives after mining the block and announcing it on the network.

• The second reward comes in the form a fee charged to the users of the network for sending transactions. The fee is given to the miners for including the transactions in a block. This fee can also be considered a miner’s income because as more and more

Bitcoins are mined, this fee will become a significant portion of the income.

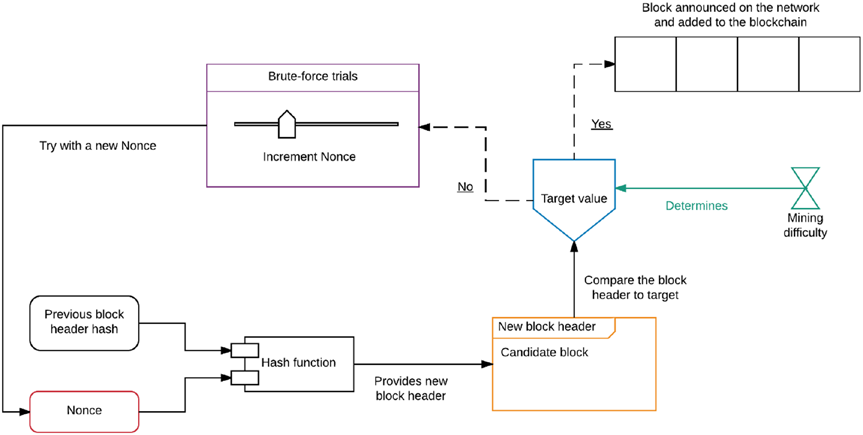

Now we can put these concepts together in the form of another flowchart, as shown in Figure 2-3. This will help solidify the process of mining in the context of difficulty and target values.

Figure 2-3. Solving the PoW problem

Miners across the network compete to solve the problem and the winning miner announces the block to the network, which then gets incorporated in the blockchain. To solve the PoW, a miner has to keep generating new hash values (through the hash function) using the incremented nonce until a hash that is below the target value is discovered. In this case, notice that the nonce is the only adjustable value. This is a simplified PoW scheme and there are small differences in its implementation.

■ Note the term mining is used because the process is similar to the mining of rare metals. it is very resource intensive and it makes new currency avaliable at a slow rate, just like the miners in the Bitcoin protocol getting rewarded.

11

Chapter 2 ■ the Gold rush: MininG BitCoin

We talked about the self-correction properties in Bitcoin network and how they allow the network to adapt. Next, we take a look at an unexpected case of having a very large number of miners in the network as Bitcoin gained popularity. This led to an arms race of sorts and it had far-reaching consequences. First, though, we need to talk about the new types of mining hardware that emerged.

Mining Hardware

As Bitcoin started to gain more popularity and acceptance with merchants, more miners joined the network in hopes of earning rewards. Miners began to get more creative with how they approached mining, such as using specialized hardware that can generate more hashes. In this section, we discuss the evolution of mining hardware as Bitcoin started to spread globally.

• CPU mining: This was the earliest form of mining available through the Bitcoin clients. It became the norm for mining in the early versions of the Bitcoin client, but was removed in the later updates because better options became accessible.

• GPU mining: This represented the next wave of mining advancements. It turns out that mining with a graphics processing unit (GPU) is far more powerful because it

can generate hundreds of times more hashes than a central processing unit (CPU).

This is now the standard for mining in most cryptocurrencies.

• FPGAs and ASICs: Field-programmable gated arrays (FPGAs) are integrated

circuits designed for a specific use case. In this case, the FPGAs were designed

for mining Bitcoins. The FPGAs are written with very specific hardware language

that allows them to perform one task very efficiently in terms of power usage and

output efficiency. Shortly after the introduction of FPGAs, a more optimized, mass—

produceable, and commercial design came out in the form of application-specific

integrated circuits (ASICs). The ASICs have a lower per-unit cost, so the units can be mass produced. The ASICs-based devices are also compact, so more of them can be

integrated in a single device. The ability of ASICs to be combined in arrays at a low price point made a very convincing case for accelerating the rate of mining.

• Mining pools: As the mining difficulty increased due to the rise of ASICs, miners realized that individually, it was not financially wise to continue mining. It was

taking too long, and the reward did not justify the resources that went into mining.

The miners then organized themselves into groups called pools to combine the

computational resources of all the members and mine as one unit. Today, joining a

pool is very common to get started with mining in almost every cryptocurrency.

• Mining cloud services: These are simply contractors who have specialized mining rigs. They rent their services to a miner according to a contract for a given price to mine for a specific time.

It is easy to see how ASICs completely changed the mining game after developers and hardware hobbiysts realized that custom arrays of ASICs can be assembled at a fairly cheap price point. It was the beginning of a kind of arms race in Bitcoin hardware, as developers were designing new chips and buying new equpiment for mining rigs that allow them to mine the most Bitcoin. This initial push, driven by profit, accelerated Bitcoin’s reach and created a golden era for the alternative currency. More developers and enthusiasts joined in, buying custom hardware to maximize their profits. The network responded by increasing the difficulty as the number of miners increased. Within a short time span, the bubble could not sustain itself for the miners due to the self-correcting features present in the protocol and the difficulty kept rising. In some cases, the hardware that miners purchased could no longer mine profitably by the time it arrived from the factory. A significant capital investment was required up front to achieve any appreciable 12

Chapter 2 ■ the Gold rush: MininG BitCoin

returns. Most of the ASICs hardware is now historic, and even Bitcoin mining pools are not profitable for the average miner. The startups and companies that commercialized ASICs and custom hardware made a decent short-term profit and then flopped. We examine a few of those massive failures in the next section.

Startup Stories

In this section, we highlight a few stories from the gold rush era of Bitcoin between mid-2013 and late 2014.

The startups covered here followed the strategy of selling pickaxes to make profits, but some took it a step further. The first startup we discuss is Butterfly Labs. This company out of Missouri came about in late 2011

with the promise of selling technology that was capable of mining Bitcoin leaps and bounds ahead of the competition. Their ASICs were supposedly able to mine Bitcoin 1,000 times faster, and they opened up for preorders soon after the initial announcement in 2012. Miners flocked to purchase the hardware, which was promised for delivery by December of the same year. Butterfly Labs collected somewhere between $20

million and $30 million in preorders as reported by the Federal Trade Commission (FTC). Shipments started to roll out to only a few customers around April 2013, but most customers did not receive their mining equipment for another year. When the customers did recieve their machines, they were obsolete, and some accused Butterfly Labs of using the hardware to mine for themselves before delivering them. Despite being unable to follow through with their initial orders, Butterfly Labs began offering a new and much more powerful miner and opened preorders for that new miner. Ultimately, the company became one of the most hated in the Bitcoin community, and the FTC had to step in to shut it down.

The second company we discuss, CoinTerra, is a more complicated case because the startup was founded by a team that had deep expertise in the field. The CEO, Ravi, was a CPU architect at Samsung previously, and the company’s board included many other leaders in the field. Initially, they were venture backed and well funded, and in 2013, they announced their first product, TerraMiner IV, which was supposed to be shipped in December of the same year. The company could not ship the product in time and eventually pushed the date back. The miner still did not arrive in 2014 and eventually CoinTerra apologized to customers, offering them some compensation, which was also largely delayed, frustrating customers even further. It seems that the company is trying to pivot to cloud mining services, but most of its customer base has already lost their trust.

The final case focuses on a startup called HashFast. Similar to previous two examples, HashFast was offering miners called Baby Jet that would be delivered in December 2013. The team at HashFast overpromised the features and underdelivered at a time when difficulty skyrocketed. It is likely that the company took the cash from early adopters to fund its own development, and when they encountered difficulties, the customers demanded refunds for their orders. The problem at the time was that the price of Bitcoin increased steadily, so the company did not have enough funds to pay back the customers. They were facing multiple lawsuits and running out of cash reserves very fast. Eventually, a judge allowed the auctioning of all assets that the company owned to pay back the creditors and investors. A common theme these companies share is that they were frequently unable to deliver mining hardware on the promised timeline and significantly delayed or refused to issue any refunds to their customers.

We can construct a general scheme of operations from the cases presented here and other ASICs startups that failed similarly to Butterfly Labs:

• Open for preorders at very high prices and falsely advertise a ridiculously high

hashing rate with a huge return on investment.

• Invest all the funding from preorders to begin research and development for ASICs and custom hardware.

• Once the mining hardware has been obtained from overseas manufacturers, use it to mine nonstop for months internally.

13

Chapter 2 ■ the Gold rush: MininG BitCoin

• Broadcast to customers through social media that the manufacturing process is

taking longer than expected.

• Deliver the hardware only to the customers that threaten to sue as early proof that shipments have begun rolling out.

• Deliver the ASICs hardware to other customers when it is already severely

out of date.

• Customers complain and file lawsuits, and the company eventually falls apart and

faces huge fines.

New Consensus

We conclude this chapter by talking about the same theme that we started it with: consensus. This chapter’s central idea was that in Bitcoin, mining is used to reach consensus to prevent users from double spending and validate all the transactions. However, since the advent of Bitcoin, other consensus algorithms have been developed. We refer to the PoW algorithm referenced in the original Bitcoin protocol for reaching consensus as the Nakamoto Consensus. A new consensus algorithm that has recently become popular is known as proof of stake (PoS), where the participants essentially play the role of validators. In Bitcoin, bad actors with fraudulent transactions have to face a rigorous approval process and validation from the network of miners. In PoS, the participants have a stake in the network (hence the name) in the form of currency.

As such, they want to see the network succeed and trust emerges in blocks that have the largest stake of currency invested by the validators. Additionally, the malicious validators will get their stake slashed for acting in bad faith. We dive into the technical aspects of PoS, and how it compares to the mechanism of PoW, later in the book. Our journey ends in this chapter with consensus and we pick up our discussion on the Bitcoin network and the blockchain in the next chapter.

Summary

In this chapter, we talked about the concept of mining and presented the technical background necessary to understand how miners verify blocks. We discussed in depth the backbone of mining in Bitcoin called PoW, and throughout the remainder of the book, we present other consensus mechanisms. Then, we described the arms race in Bitcoin mining over producing the best hardware, which led to the huge rise in difficulty, and the startup failures that resulted from that time period. Finally, we ended the chapter with a mention of PoS, which we return to in a later chapter.

References

The key references used in preparing this chapter were Michael Nielsen’s post (http://www.

michaelnielsen.org/ddi/how-the-bitcoin-protocol-actually-works/) on Bitcoin mining, and Aleksandr Bulkin’s post (https://keepingstock.net/explaining-blockchain-how-proof-of-work-enables-

trustless-consensus-2abed27f0845). The remaining references can be found at the end of the book.

14