The global financial markets are undergoing a drastic change that makes it clear that without innovation most business and financial models could soon become obsolete. A recent overview of the global financial system described the current system as a:

system that moves trillions of dollars a day and serves billions of people, but the system is rife with problems, adding cost through fees and delays, creating friction through redundant and onerous paperwork, and opening up opportunities for fraud and crime.

To the best of our knowledge, 45 percent of financial intermediaries, such as payment networks, stock exchanges, and money transfer services, suffer from economic crime every year; the number is 37 percent for the entire economy and only 20 percent and 27 percent for the professional services and technology sectors respectively. It’s no small wonder that regulatory costs continue to climb and remain a top concern for bankers. This all adds cost, with consumers ultimately bearing the burden. 1

Dan Tapscott pointed out that our financial system is inefficient for a multitude of reasons. Three specific realities are:

First, because it’s antiquated, a kludge of industrial technologies and paper-based processes dressed up in a digital wrapper. Second, because it’s centralized, which makes it resistant to change and vulnerable to systems failures and attacks. Third, it’s exclusionary, denying billions of people access to basic financial tools. Bankers have largely dodged the sort of creative destruction that, while messy, is critical to economic vitality and progress. ”2

We begin this chapter with issues related to the global financial markets and why blockchain can be an innovative solution for efficiencies in the financial markets. Then we move to the topics of venture capital, ICOs, cryptocurrencies, tokens, and exchanges. We address the significant ICO market impact, state 1https://hbr.org/2017/03/how-blockchain-is-changing-finance

2http://hrb.org/2017/03/how-blockchain-is-changing-finance

© Vikram Dhillon, David Metcalf, and Max Hooper 2017

183

V. Dhillon et al., Blockchain Enabled Applications, https://doi.org/10.1007/978-1-4842-3081-7_12

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

of regulation, Securities and Exchange Commission (SEC) involvement, unique technologies, business models, RegTech, and related issues. As we review these concepts and issues there are several questions and thoughts to hold in mind:

• How does crowdfunding scale blockchain applications?

• How can new companies and lending platforms be created?

• Can RegTech answer the need in the market for efficient compliance?

• What is the market impact of FinTech for banking and investment banking?

• What is the state of ICO fundraising and the ICO bubble?

• How can people of all levels of wealth participate in financial markets as technology helps democratize financial opportunities?

We close the chapter with the state of multiple large financial groups and their state of involvement in blockchain, FinTech, and other financial technologies.

State of the Blockchain Industry

The state of the blockchain industry indicates massive growth in the second quarter of 2017. According to Smith & Crown, this proved to be a period of growth across the Blockchain industry. The cryptotokens markets rose, doubling and tripling in value in the span of a few weeks. The Smith & Crown Index (SCI) over this quarter reflected a bull market, more than doubling in value between April and June. The growth of capitalization in cryptotoken markets was accompanied by a frenzy of activity in the token sale market. By all accounts, the second quarter of 2017 has been a record-setting period. 3

Blockchain Solution

As we have stated in previous chapters, blockchain is an innovative solution for disrupting the inefficiencies in the financial system. Kastelein noted that there are five basic principles underlying the blockchain technology that allows blockchain to change how financial market transactions are created. It’s worth repeating here the five basic principles underlying the technology:

• Distributed database: Each party on a blockchain has access to the entire database and its complete history. No single party controls the data or the information.

Every party can verify the records of its transaction partners directly, without an

intermediary.

• Peer-to-peer transmission: Communication occurs directly between peers instead of through a central node. Each node stores and forwards information to all other

nodes.

• Transparency with pseudonymity: Every transaction and its associated value are visible to anyone with access to the system. Each node, or user, on a blockchain has a unique 30-plus-alphanumeric address that identifies it. Users can choose to remain

anonymous or provide proof of their identity to others. Transactions occur between

blockchain addresses.

3https://www.smithandcrown.com/categories/feature/

184

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

• Irreversibility of records: Once a transaction is entered in the database and the accounts are updated, the records cannot be altered, because they’re linked to every transaction record that came before them (hence the term chain). Various computational

algorithms and approaches are deployed to ensure that the recording on the database

is permanent, chronologically ordered, and available to all others on the network.

• Computational logic: The digital nature of the ledger means that blockchain transactions can be tied to computational logic and in essence programmed. Users

can therefore set up algorithms and rules that automatically trigger transactions

between nodes. 4

Tapscott stated:

For the first time in human history, two or more parties, be they businesses or individuals who may not even know each other, can forge agreements, make transactions, and build value without relying on intermediaries (such as banks, rating agencies, and government bodies such as the US Department of State) to verify their identities, establish trust or perform the critical business logic—contracting, clearing, settling, and record-keeping tasks, that are foundational to all forms of commerce. 5

Blockchain applications can reduce transaction costs for all participants in an economy via peer-topeer transactions and collaboration. Blockchain is truly a game-changing financial markets solution using new technology and empowered by thought leadership.

Venture Capital and ICOs

The real question is this: Will ICOs supplant traditional venture capital as a fundraising model? Few could ever imagine that in one year the venture capital industry could be outpaced and changed by new innovative methods of fundraising called ICOs. ICOs, also known as token sales, came together as blockchain technology, crowdfunding, innovative wealth ideas, and cryptocurrencies investing developed new models.

ICOs are both a threat and an opportunity for the venture capital industry.

The traditional venture capitalist sees opportunities in ICOs for profits from cryptocurrency, blockchain investments, liquidity, and potential for faster financial gains. There might be a disruption in the way traditional venture capitalists operate and their position in the market. This is a great concern and time of change in the financial markets driven by technological innovation. The SEC recently asserted in a letter that ICOs are subject to security laws. The certainty that the SEC will act on cryptocurrency issues and ICOs clears up one big question. However, it is unclear how individuals, groups, and offerings become SEC

compliant. The process will take time to resolve and for rules and precedents to be established.

Initial Coin Offerings

An ICO is a means of crowdfunding the release of a new cryptocurrency. Generally, tokens for the new cryptocurrency are sold to raise money for technical development before the cryptocurrency is released. Unlike an initial public offering (IPO), acquisition of tokens does not grant ownership in the company developing the new cryptocurrency. Unlike an IPO, there is no (comprehensive) government regulation of an ICO.6

4https://hrb.org/2017/03/what-initial-coin-offerings-are-and-why-vc-firms-care

5https://hrb.org/2017/03/how-blockchain-is-changing-finance

6https://en.wikipedia.org/w/index.php?title=Initial_coin_offering&oldid=784220634

185

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

ICOs and new funding models using distributed ledger methodologies are starting to disrupt both public markets (IPOs) and private investments (venture capital). An article from Coin Desk illustrated the blockchain’s impact on venture capital formation. Coin Desk further noted, “There is proven demand and interest from both the entrepreneurial and investor audiences and limited regulatory guidance. ICOs could continue to gain steam as a funding mechanism. ”7

“Initial Coin Offerings (ICOs) are changing the cryptocurrency markets in rapid and expanding ways. Additionally, the venture capital industry is trying to understand this new financial investment. The bitcoin community created the situation by a convergence of blockchain technology, new wealth, clever entrepreneurs, and crypto-investors who are backed by blockchain-fueled ideas,” stated Harvard Business Review writer Richard Kastelein. 8

ICOs are dominating the overall crowdfunding charts in terms of funds raised, with half of the top 20 raises coming from the crypto community. The companies, such as Goldman Sachs, Nasdaq, and Intercontinental Exchange, the U.S. holding company that owns the New York Stock Exchange, which dominate the IPO and listing business, have been among the largest investors in blockchain ventures. 9

An ICO is explained by Coin Telegraph as

a recently emerged concept of crowdfunding projects in the cryptocurrency and bBlockchain industries. When a company releases its own cryptocurrency with a purpose of funding, it releases a certain number of cryptotokens and then sells those tokens to its intended audience, most commonly in exchange for Bitcoins, but it can be fiat money as well. As a result the company gets the capital to fund the product development and the audience members get the crypto tokens share, plus, they have complete ownership of these shares. 10

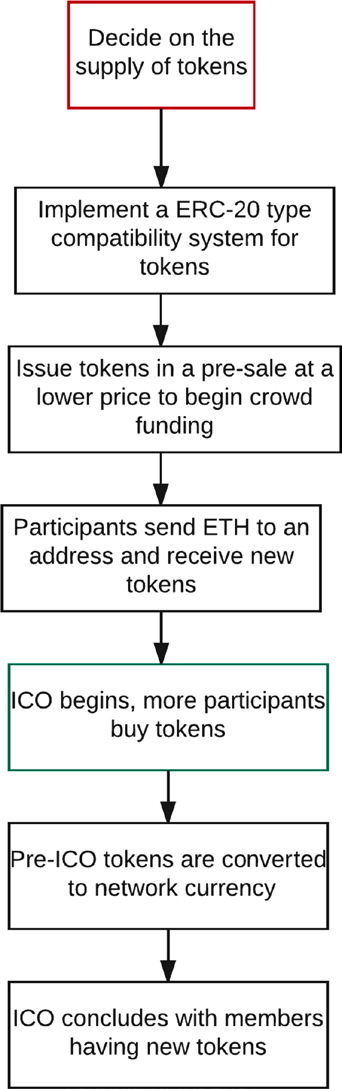

A specific example of how an ICO is created and the steps for execution are described in the SONM

execution model. First of all, what is SONM? “SONM is a global operating system that is also a decentralized worldwide fog computer. It has the potential to include unlimited computing power (IoE, IoT). Worldwide computations organized using the SONM system can serve to complete numerous tasks from CGI rendering to scientific computations.” 11

The defining feature of SONM is its decentralized open structure, where buyers and workers can interact with no middleman, while building a market profitable for them first, unlike other cloud services (e.g., Amazon, Microsoft, Google).

Unlike widespread centralized cloud services, the SONM project implements a fog computing structure, a decentralized pool of devices, all of which are connected to the Internet (IoT/IoE).

SONM is implemented using the SOSNA architecture for fog computing.

The specific execution steps in the SONM ICO are as follows:

• The SONM platform uses a token of the same name, SONM (ticker SNM).

• Total supply of SNM will be limited to the amount of tokens created during the

crowdfunding period.

7https://www.coindesk.com/ico-investments-pass-vc-funding-in-blockchain-market-first/

8http://hrb.org/2017/03/what-initial-coin-offerings-are-and-why-vc-firms-care

9http://hrb.org/2017/03/what-initial-coin-offerings-are-and-why-vc-firms-care

10https://cointelegraph.com/explained/ico-explained

11https://sonm.io/Somn-BusinessOverview.pdf

186

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

• SNM tokens will be used by the computing power buyers to pay for the calculations using the smart-contracts-based system.

• SNM is a token issued on Ethereum blockchain using standards of implementation

and storage and management of tokens including Ethereum wallet.

• SONM project crowdfunding, ICO, and SNM creation will take place using Ethereum

smart contracts.

• Participants willing to support the SONM project development will send Ether to

a specified ICO Ethereum address creating SNM tokens by this transaction at the

specified SNM/ETH exchange rate.

• ICO participants will be able to send Ether to the SONM crowdfunding Ethereum

address only after the start of the crowdfunding period (specified as the Ethereum

block number).

• Crowdfunding will finish when the specified end block is created or when the ICO

cap is reached.

• SNM tokens sale ICO.

• SONM presale launched on April 15, 2017, and was successfully finished in less than 12, hours raising 10,000 Ethereum.

• Pre-ICO tokens will be transferred into the main token contract through a special safe migration function.

• Token allocations are completed to all parties.

• Transaction is complete.12

12https://sonm.io/Somn-BusinessOverview.pdf

187

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

This process is shown in Figure 12-1.

Figure 12-1. ICO process for the SONM token illustrated visually

188

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

Digital Currency Exchanges

Digital currency exchanges (DCEs) or Bitcoin exchange are businesses that allow customers to trade digital currencies for other assets, such as conventional fiat money, or different digital currencies. They can be market measures that typically take the bid–ask spreads as transaction commissions for their services or simply charge fees as a matching platform. 13

Typically DCEs operate outside of Western countries, avoiding regulatory oversight and complicating prosecutions. A U.S.-based global Bitcoin exchange named Kracken is located in San Francisco. The Kracken web site says Kracken is the world’s largest global Bitcoin exchange in Euro volume and liquidity. Poloniex is described on its web site as a U.S.-based digital asset exchange offering maximum security and advanced trading features.

As one works with DCEs and for all aspects of operating in the world, it is very important to establish identity easily and exactly. The future of identity management looks different with blockchain technology in a decentralized digital world. Digital identity networks built on blockchain drives trust among businesses as a social enterprise by leveraging shared ledgers, smart contracts, and governance to standardized management, at the same time reducing the cost, risk, time, and complexity of decentralized identity management.

Status of ICO Regulation

At this time, Coin Desk discusses the state of ICO regulation with a focus on legal status in six nations.

Several points of interest are quoted by a recent report from Autonomous Next, a FinTech and research firm. The report considers Switzerland and Singapore to be the two most advanced nations for creating welcoming environments for FinTech and cryptocurrencies. In Switzerland, the law is that cryptocurrencies are assets rather than securities. The same is true for Singapore. The Singapore MAS authority does not regulate virtual currency transactions, but does monitor KYC and AML, the report states.

The report singled out the United Kingdom and United States as jurisdictions with high activity, but a lack of legal clarity. The United States, with many regulatory groups and 50 states that implement rules, makes the process of regulation more complex. The state of Delaware has recently passed blockchain-related legislation. In China, tokens are considered a nonmonetary digital asset. Russia has been welcoming of cryptocurrencies. Cryptotokens are categorized as legal financial instruments similar to derivatives.14

Smith & Crown stated a significant problem in the legal status of token sales still being in question.

Participants in token sales might not enjoy the same legal status or protections as investors in private and public equity sales. Uncapped token sale raises and structures that allow projects to raise large sums of capital while retaining majority control over their token economy could exacerbate this problem by drawing attention from regulatory agencies. A number of countries are actively exploring new regulatory frameworks for token sales, and several groups, including Smith & Crown, are developing guidelines for best practices and self-regulation.15

The current regulation status is that the SEC in the United States issued a letter stating that ICOs, cryptocurrencies, and related matters are viewed by the SEC as securities. As stated previously, this brings some clarity to the marketplace on this issue. Although some will read it positively and others negatively, ultimately the SEC statement set in motion an entirely new understanding of the regulatory environment both in the United States and globally.

13https://en.wikipedia.org/wiki/Digital_currency_exchange

14https:www.coindesk.com/state-ico-regulation-new-report-outlines-legal-status-6-nations/

15https://www.smithandcrowm.com/quarter-two-review

189

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

A Securities Law Framework for Blockchain Tokens describes multiple key thoughts and actions for anyone that is interested in blockchain tokens. “The Framework focuses on US federal securities laws because these laws pose the biggest risk for crowd sales of blockchain tokens. In many jurisdictions, there may also be issues under anti-money laundering laws and general consumer protection laws, as well as, specific laws depending on what the token actually does.” The Howey Test establishes the test for whether an investment contract is a security ( SEC v. Howey).16

The framework illustrates six best practices for token sales:

1.

Publish a detailed whitepaper.

2.

For a presale, commit to a development roadmap.

3.

Use an open, public blockchain and publish all codes.

4.

Use clear, logical, and fair pricing in the token sale.

5.

Determine the percentage of tokens set aside for the development team.

6.

Avoid marketing the token as an investment.

Pros and Cons of ICO Investments

The pros and cons of investing in ICOs are illustrated by Jim Reynolds in a recent article from “Invest It In: Investment Ideas.” This list of pros and cons is by no means exhaustive, but it does contain many points to consider.

The following are the pros of ICOs.

For ICO Founders: Entrepreneurs

• Raise capital efficiently.

• ICOs are much cheaper than IPOs.

• ICOs require much less documentation than IPOs.

• Branding and marketing opportunity to get exposure for an altcoin.

• Community building.

• Create skin in the game with early adopters; this will make them part of the

marketing mechanism of the project.

• Entrepreneurs share both the risks and the benefits of their efforts with the investors.

• Founders/developers have a method that can help them finance a project that can

make the best use of their skills to the maximum possible extent.

• Well-respected crypto-experts have a channel to cash in on the skills and credibility they built over the years.

• Proof of stake altcoins resolve the problem of fair distribution through ICOs, and in PoS the coins come to fruition immediately.

16https://www.coinbase.com/legal/securities-law-framework.pdf

190

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

• Venture capital funding is much more intrusive on the founder’s Vision360. An

alternative to an ICO is borrowing, but this has many implications on the project

cash flow that is not always possible to manage in altcoin/crypto projects.

• Some transparency; for example, an escrow can be used to verify how the funds are being spent after the ICO.

• Early investors will have more liquidity in early-stage companies.

• Early access to a token that has the potential for capital growth.

• Not regulated or registered with any government organization and there are usually no investor protections other than what is built into the platform itself.

• Investors can be part of a community.

• An innovative way to deploy capital.

• An ICO that uses existing networks such as Stratis, Ardor, and Ethereum, is tapping into the network capital of an existing ecosystem.

• Divest from main cryptocurrencies into altcoins.

• Investors are usually the first users of the altcoin; thus, unlike holding a stock of a company whose products an investor never used, ironically altcoins can be more

tangible than other investments.

• The returns from investing in ICOs can be up to 1,000 percent, and also could be

complete losses.

• Diversification into other assets.

• A high-risk, high-reward investment which is (to some extent) disconnected from

the stock market and the economy.

• Own an alternative asset not based on fiat currency.

For the Cryptocurrency Community

• Altcoins will fuel the race to build Web 3.0, a decentralized web. The Internet stack becomes fully independent from any central entity.

• Altcoins are the cutting edge of FinTech, even if an altcoin project technology fails.

There will be lessons learned regarding the technology and business model being

proposed that will benefit the whole community.

• More competition in the crypto space makes the competitors leaner, meaning the

“invisible hand” of the market frets much faster in terms of creative destruction and survival of the fittest the more altcoin projects are launched.

• Intra-altcoin competition is healthy, as it prepares the altcoins for the real

competition, the crypto-based decentralized projects vs. traditional firms.

• There are two schools of thought: Bitcoin maximalists who consider Bitcoin as the one and only true cryptocurrency and altcoins as experiments. Others think the

altcoins will eventually replace Bitcoin, just like the video was replaced by the CD, Myspace by Facebook, and old cameras by digital ones.

191

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

The following are the risks of investing in ICOs.

• Scammers take advantage of an unregulated industry.

• Amateurs can use ICOs to launch projects that are doomed to fail.

• Long project delivery timelines increase the risk that competitive products will be launched before.

• Exchanges need to accept the altcoin for there to be a market for the altcoin.

• An ICO can be surrounded by hype, and “pumping” to mask the cons of the ICOs

and make investors invest emotionally, only to find out later that it was all hot air.

This is done by piggybacking on the success of Bitcoin, Ethereum, and Dash without

offering anything real back in return.

• Regulators can change rules and make coins with certain functionality illegal in the future.

• Altcoin technology is extremely new, and basic issues such as agreement on

protocols are not yet established. Many altcoins will be born, and others will

dissipate in the past until we eventually see the Google, Facebook and YouTube of

cryptocoins.

• Certain tokens can be copied (forked) and made better. The clone can eventually

have more value than the original. This happens when the token is not an intrinsic

part of the network. 17

Regulation Technology: RegChain

Regulation technology (RegTech) is a new innovation area that holds great promise for the regulation industry. RegTech is defined by Investopedia as “a blend word of regulating technology” that was created to address regulatory challenges in the financial services sector through innovative technologies. RegTech consists of a group of companies that use technology to help businesses comply with regulations efficiently and inexpensively.18

A summary in EY’s publication “Innovating with Reg Tech” illustrates several benefits offering regulation technology:

• Supports innovation.

• Provides analytics.

• Reduces cost of compliance.

There are also some short-term benefits:

• Cost reduction.

• Sustainable and scalable solutions.

• Advanced data analytics.

• Control and risk platforms to be linked seamlessly.

17https://www.investitin.com/crypto-ico-pros-cons/

18www.investopedia.com/terms/r/regtech.asp

192

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

Long-term benefits include the following:

• Positive customer experience.

• Increased market stability.

• Improved governance.

• Enhanced regulatory reporting. 19

A current innovation experience of a RegTech model created by Deloitte is RegChain.

Deloitte, in collaboration with Irish Funds and their members, advanced “Project Lighthouse” to assess blockchain technology’s ability to service regulatory reporting requirements. The project tested the ability for a platform to provide individual nodes for fund administrators to store and analyze fund data while coding regulatory reporting requirements into smart contracts for execution and data validation. A regulator node was also facilitated, allowing the safe and secure exchange of data between firms and the regulator, as well as to increase overall reporting efficiency and market transparency.

In addition to technical design and development, a comparative business analysis was undertaken to review the cost–benefit analysis of the proposed blockchain solution.

RegChain was developed using Deloitte’s rapid prototyping process, which uses an experiment-driven agile methodology. Key phrases included solution visioning definition of design and test parameters, development sprints, and ongoing reviews with an

industry subcommittee with participants from across the fund administrator and fund management world.

A key consideration and cornerstone for this project was to ensure collaboration among technologists and industry representatives from operations, regulatory teams, and senior management. This was deemed critical in order to have a comprehensive PoC design, and moreover, to help define how a future production solution could be realized. 20

Blockchain technology was used due to a number of features and characteristics that can enhance the overall ability to meet reporting requirements:

• Data integrity.

• Reliability.

• Storage and speed.

• Analytics.

• Proof-of-concept (PoC).

The PoC created RegChain, a blockchain-based platform that streamlined the traditional regulatory reporting processes by acting as a central repository for the safe storage and review of a large volume of regulatory data. RegChain has been used in the marketplace successfully in multiple applications and gives hope that the future will see wider adoption and enjoy the benefits of this model.

19https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/financial-services/performancemaga-

zine/articles/lu_RegChain%20Reaction_Performance23.pdf

20https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/financial-services/

performancemagazine/articles/lu_RegChain%20Reaction_Performance23.pdf

193

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

New Blockchain Companies and Ideas

A Harvard Business Review article states, “Many businesses have yet to make the leap from the Industrial Age to the Information Age, and the gap between technological and organizational progress is widening. ”21

Goldman Sachs has taken a series of steps that are bold and decisive in the area of digital innovation and blockchain applications. Goldman has been involved in some blockchain technology-based companies like Circle and Digital Assets Holdings. Additionally, in October 2016 Goldman Sachs introduced an online platform offering unsecured personal loans to consumers.

Homechain and SALT

Another new company is Homechain, described as the future of loan origination and regulatory compliance.

The business idea is reducing the home loan origination and regulatory compliance process from 42 days to 5 days. RegChain allows for compliance to reporting bodies.

At this time, blockchain technology is at the stage where the Internet was in 1992, and it is opening up a wealth of new possibilities that have the promise to add value to numerous industries, including finance, health, education, music, art, government, and more. 22

The SALT lending platform allows the holders of blockchain to leverage their holdings as collateral for cash loans. SALT is the first asset-based lending platform to give blockchain asset holders access to liquidity with them having to sell their tokens. SALT provides investors an innovative and secure opportunity to lend against a high-growth asset class through a fully collateralized debt vehicle. SALT is traditional lending secured by nontraditional collateral.

Each SALT token is representative of a membership to the SALT Lending Platform. The token is an ERC20 smart contract.

Blockchain technology is making waves in many industries. Companies in various sectors are innovating and using blockchain to create new applications and start up disruptive companies. A report by Accenture shows the cost data of eight of the world’s largest investment banks, and states that blockchain technology could help reduce the costs of investment banks by as much as $12 billion per annum by 2025.

There are multiple benefits for investment banks using blockchain technology, including safer data, more secure data, and cost reductions. 23

Ambrosus, Numerai, and SWARM

Another example of a new company that was recently created is a Swiss blockchain company, Ambrosus.

This company was launched to employ smart contracts to track food quality. Innovation using blockchain technology is being adapted everywhere.

Numerai is a new kind of hedge fund built by a network of data scientists. Numerai is a crowdsourced hedge fund for machine learning experts. In the first year of collection, 7,500 data scientists created algorithms on the Numerai platform as reported by Tech Crunch. Numerai announced Numeraire, a cryptocurrency token to incentivize data scientists around the world to contribute AI. The Numerai smart contract was deployed to Ethereum and more than 1.2 million tokens were sent to 19,000 data scientists around the world, as reported by Numerai.24

The startup company Swarm advanced several new concepts into the marketplace and was at the leading edge of two emerging concepts, crowdfunding and cryptocurrency, while creating a startup in a market with complex and evolving regulations. The idea was to transform the way entrepreneurs raise money. Swarm created a new idea called crypto-equity, a token that represents the success of your project.

21https://hbr.org/2017/03/how-blockchain-is-changing-finance

22https://hbr.org/2017/03/how-blockchain-is-changing-finance

23https://saltlending.zendesk.com/hc/en-us/sections/115002568808-Technology

24https://medium.com/numerai/an-ai-hedge-fund-goes-live-on-ethereum-a80470c6b681

194

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

Swarm was built on the following three components:

• Crypto-equity.

• Crowdsourced due diligence.

• Coins distributed to all Swarm holders. The best description of Swarm is like a

crypto-Kickstarter offered via coins.

KICKCO is a new company with a unique model. Their web site states:

KICKCO sits at the intersection of two young industries: blockchain and crowdfunding.

KICKCO moves crowdfunding from centralized platforms such as Kickstarter, to Ethereum-based smart contracts. This not only allows us to implement the crowdfunding model in a decentralized way—significantly reducing overhead—it also provides a mechanism to protect backers from failed projects—guaranteeing their investment with blockchain based tokens called KickCoins. KICKCO will provide users with a powerful, convenient, and up to date platform for both ICO and crowdfunding campaigns. KICKCO is a site for automated and independent ICOs, pre-ICOs, and crowdfunding campaigns built

on Ethereum and funded by cryptocurrencies. The purpose of KICKCO is to solve the aforementioned problems and create a single platform that will unite the creators and backers of ICO and crowdfunding campaigns to form an active up to date community.25

The companies that have been described show some of the innovation and creative thought that works around the blockchain models. The blockchain continues to advance new and exciting ways for financial markets to become more efficient.

Democratizing Investment Opportunities

Blockchain can help the world’s poorest people. A World Economic Forum article described the way that transactions can be recorded in an inexpensive and transparent way, allowing for money to be exchanged without fear, fraud, or theft. Blockchain smart contracts, sending money internationally, reducing costs, insurance services, helping small businesses, humanitarian aid, and blockchain-powered identity systems are just some of the ways blockchain can help many people. For those without passports, birth certificates, phones, or e-mail, blockchain records can speed processing, allowing for a better way of life for many people.

Through crowdfunding smaller investment amounts and many new capital formation ventures, people who have previously not had the opportunity for sharing in the economies of a growing financial market can participate. Blockchain helps to democratize finance and affect lives in new ways.

25https://www.kickico.com/whitepaper

195

Chapter 12 ■ teChnologiCal revolutions and FinanCial Capital

Summary

The future is for creation, innovation, change, and global impact as crowdfunding enables blockchain on a global scale. Reports from both EY and Innovate Finance delve into the capital markets landscape. Chris Skinner, in his blog, “Fintech and the World of Investment Banking,” stated that, “there is a raft of new technologies that are architecting the landscape of capital markets and hundreds of startups leveraging these new technologies to both assist and attack the inefficiencies in the investment banking world. Rather than ignoring these changes the biggest banks are investing in them. ”26

Goldman Sachs, Citicorp, JPMorgan, Morgan Stanley, Wells Fargo, and Bank of America are just some of the large banks and investment bankers investing millions in FinTech, blockchain, and other technology innovations.

Disruption in the capital markets is moving at a rapid pace. A recent Forbes article indicated that there are more than 900 cryptocurrencies in existence now, with more being added each day. The ICO market has raised more money than the venture capital market in the last six months as of mid-2017. There will be many future market ups and downs, with new regulations coming to the market, and many changes on the way as we experience technological revelations and financial capital changing rapidly.

A special salute goes to the innovators, dreamers, individuals, and groups that are in the marketplace and see the future of a better financial world for everyone. The incredible commitment of incubators, accelerators, universities, and investment firms working toward blockchain efficiencies and innovation will change the way the world views financial capital.

Examples of innovation are everywhere. Goldman Sachs, JPMorgan, Nasdaq, and special alternative investment firms such as Triloma Securities offer unique products, services, innovation, and capital. What is occurring in many local markets is a collaboration of groups configured and aligned working together for common goals in the technology area. One unique group in the Orlando and central Florida area has come together to help startups and advance blockchain research and applications. This group is comprised of various organizations including Florida Angel Nexus, Merging Traffic, StartUp Nations Ventures, Institute of Simulation & Training, METIL (Mixed Emerging Technology Integration Lab), the Medical Tourism Association, and many others, all working in a robust public–private partnership ecosystem that drives change for the good of all in the marketplace.

Blockchain will bring a unique technological revolution in financial capital.

26https://www.thefinanser.com/2017/08/fintech-world-investment-banking-html/

196